|

◇Another FSS Revision Request Delays AriBio Merger Again

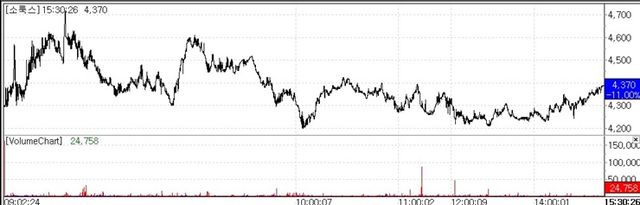

Shares of Solux fell 11.0% to KRW 4,370 on July 3, according to KG Zeroin's MP Doctor, after the FSS requested revisions to the company's securities registration statement related to its planned merger with AriBio.

The regulator cited deficiencies in the filing format, omissions or misstatements of material information, and descriptions that could hinder investors' ability to make informed decisions. As a result, the registration statement is deemed not accepted, effectively putting the merger process on hold until a revised filing is submitted.

The market reacted strongly because investors had viewed the latest filing as a sign that the nearly two-year merger process was finally entering its final stage. In the June 23 filing, Solux and AriBio proposed holding a shareholder meeting to approve the merger on August 25, completing the merger on September 29, and listing new shares on October 21. The filing also updated the valuation of the surviving entity, Sorux, to KRW 533.1 billion and AriBio to KRW 551.0 billion.

However, the FSS requested another revision only nine days after the filing, reigniting concerns that the merger could face further delays. Since the deal was first announced in 2024, the companies have repeatedly revised their filings and postponed the transaction timeline.

Industry observers believe regulators continue to scrutinize the valuation methodology used for AriBio. The company's lead pipeline, AR1001, is an oral Alzheimer's disease treatment currently in global Phase 3 clinical trials. Because the drug has yet to receive regulatory approval, authorities appear to be taking a cautious approach toward assumptions involving future revenue projections, technology valuation, and commercialization agreements, including licensing deals in China and distribution rights in the UAE.

The latest revision request is also expected to delay the overall transaction schedule. Under Korea's Capital Markets Act, the company must submit a revised registration statement within three months. Otherwise, the filing will be deemed withdrawn. As a result, the planned extraordinary shareholders' meeting in July and the merger approval process scheduled for August are likely to be postponed.

◇AprilBio Continues to Slide Despite TKG Acquisition

AprilBio closed down 6.7% at KRW 32,700, extending its losing streak to four consecutive trading sessions. The stock has now fallen 20.7% since June 30.

Perhaps the most striking development is that the current share price has fallen well below the transaction price agreed upon by the new investors. TKG HucHems will acquire convertible preferred shares with a conversion price of KRW 42,953, while IMM's common share subscription price is KRW 40,908. The market price is now trading roughly 27% and 23% below those respective levels.

The deal will inject KRW 346.8 billion into AprilBio, increasing the company's cash holdings to around KRW 400 billion. Korea Investment & Securities maintained its Buy rating and KRW 112,000 target price following the announcement, arguing that the company's valuation remains attractive given its enlarged cash position.

Nevertheless, investors appear to be focusing less on the capital injection itself and more on whether the new funding can translate into higher corporate value. AprilBio has successfully licensed out assets based on its SAFA platform to Lundbeck and Evommune, but no additional major licensing deals have followed. Investors are now waiting to see whether the newly secured capital will accelerate pipeline development and generate another global partnership.

Some market participants also cited potential dilution from the convertible preferred shares and short-term profit-taking as additional factors weighing on the stock.

◇LnC Bio Weakens Despite Positive U.S. Expansion Story

LnC Bio also traded sharply lower, falling 5.25% to KRW 83,100. Despite ranking among the biggest decliners in the biotech sector during the session, the stock recovered some of its losses before the close.

The company said there were no internal issues behind the decline.

"There are absolutely no company-specific issues, and all business operations are proceeding as planned," an LnC Bio official said. "We have also checked with market participants, and there are no known negative rumors or undisclosed issues. Given the strong share price appreciation in recent months, today's move appears to be largely driven by profit-taking, although the decline itself seems excessive."

Fundamentally, the company's outlook remains positive. Sales of its extracellular matrix(ECM)-based skin booster Rituo continue to accelerate. Hana Securities expects second-quarter Rituo sales to nearly double from the first quarter to approximately KRW 14 billion, while forecasting 92% year-over-year revenue growth and a significant improvement in operating profit this year.

LnC Bio's long-term growth story also remains intact. The company is preparing to enter the U.S. human tissue graft market by establishing a U.S. subsidiary and local manufacturing facilities. It recently secured a key U.S. patent related to human tissue graft technology, while recent legislative changes in Korea have also created a legal framework for commercializing processed human adipose tissue, opening another potential growth avenue.

Market participants therefore believe the decline reflected short-term technical selling rather than deteriorating fundamentals. Rituo's continued sales growth, expansion into the U.S. market, and commercialization of adipose tissue-derived products remain the company's primary long-term growth drivers.

Overall, the sharp sell-off across the biotech sector appeared to be driven more by weakening investor sentiment than by company-specific fundamentals. Even companies supported by government funding, licensing expectations, strategic acquisitions, and overseas expansion failed to escape the downturn, suggesting that investors are increasingly demanding tangible business execution—rather than headline announcements—to support higher valuations.

Copyright ⓒ 이데일리 무단 전재 및 재배포 금지

본 콘텐츠는 뉴스픽 파트너스에서 공유된 콘텐츠입니다.

다음 내용이 궁금하다면?

광고 보고 계속 읽기

원치 않을 경우 뒤로가기를 눌러주세요