The temporary deterioration in investor sentiment triggered by Alteogen, the largest company by market capitalization on the KOSDAQ, appears to have shifted into a wait and see mode. On the KOSPI RNA drug developer Samyang Biopharm posted strong gains.

|

◇"Merck Royalties, Extended Contract Duration and Stronger Revenue Taken Into Account

Alteogen the No. 1 KOSDAQ company by market capitalization which boasted a market cap of won 29 trillion at the end of last year, saw its valuation slide to the won 19.7 trillion range as of the 22nd. Nearly won 10 trillion in market value evaporated in a month.

According to KG Zeroin MP Doctor, Alteogen closed the day at won 370,000, down 0.94% (won 3,500) from the previous session, following a sharp plunge of 22.35% (won 107,500) the day before.

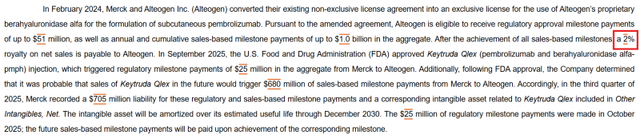

The reason approximately won 6 trillion in market capitalization disappeared in a single day was that, in Alteogen’s largest technology transfer agreement—its deal with Merck (MSD)—the royalty rate was revealed to be 2%, rather than the roughly 5% level the market had been expecting.

Alteogen is the partner that converted MSD’s immuno-oncology blockbuster Keytruda (pembrolizumab) from an intravenous (IV) formulation to a subcutaneous (SC) formulation. Keytruda is the world’s best-selling blockbuster drug, with annual sales of USD 29.5 billion (approximately won 43 trillion) in 2024 and estimated sales of USD 31.0 billion (approximately won 45.5 trillion) last year.

MSD's SC formulation, Keytruda Qlex, developed in collaboration with Alteogen, received approval from the U.S. Food and Drug Administration (FDA) in September last year. Under the contract terms, Alteogen is eligible to receive milestone payments each time MSD achieves certain sales thresholds with Keytruda Qlex, and thereafter will receive a fixed percentage of net sales as royalties.

While Alteogen had consistently maintained that it could not disclose the royalty rate under the contract, MSD's third-quarter Form 10-Q filed with the U.S. Securities and Exchange Commission (SEC) in November last year stated the royalty rate as 2% of net sales. This information was belated made known in the local market on 21st.

Assuming that 50% of existing Keytruda patients switch from the IV formulation to the SC formulation, Alteogen is expected to receive approximately won 430 billion annually in royalties at a 2% rate a significant gap from what the market had speculated for at the 5% royalty rate.

In a statement released on the 22nd, Alteogen said, “Royalties are matters that must not be disclosed without mutual consent between the two parties,” adding, “With regard to this issue, our legal team has been reviewing the matter together with external legal advisors and has been continuing discussions with MSD on follow-up measures.”

Alteogen continued, “As this issue suddenly became public while such discussions were ongoing, we apologize for not being able to immediately deliver a sufficiently organized message to the market.”

It added, “Once the discussions are concluded and the scope of information that can be disclosed regarding follow up measures is determined, we will share it promptly and transparently with the market and our shareholders.”

|

In further explanation, Alteogen stated, “Alteogen’s ALT-B4 material patent remains valid in the United States until early 2043, allowing royalties to be received over a long period.”

The company added, “The contract between our company and MSD took into account the uncertainty that Alteogen’s technology had not yet been commercialized at the time of signing,” and said, “The royalty with MSD reflects a contract term approximately 1.8 times longer than typical licensing agreements, as well as a large sales base and milestone scale.”

Alteogen emphasized, “This contract will enable stable and substantial cash inflows over a long period of time.”

and added “Subsequent contracts have negotiated royalties within ranges commonly accepted in the industry, and future agreements will also be concluded at standard royalty levels.”

|

◇Samyang Biopharm’s RNA platform drives valuation

Samyang Biopharm, which relisted following a spin-off from Samyang Holdings, closed the day at won 92,900, up 23.21% (won 17,500) from the previous session.

A Samyang Biopharm representative told Edaily that, “We were unable to determine a clear reason for the abrupt stock price movement,” adding, “The most recent news communicated to the market was our selection for a KDDF research project.”

Samyang Biopharm had been absorbed by Samyang Holdings in 2021 and operated as an in-house independent company (CIC). It was spun off and relisted on November 24 last year for its standalone value to be properly recognized by the market. On its first trading day, Samyang Biopharm closed at won 30,200, up won 6,950 (29.89%). In just about two months since then, its corporate value has tripled.

Samyang Biopharm is concentrating its R&D capabilities in three areas; improved drugs applying drug delivery technologies, innovative biologics that will lead future cancer therapies, and medical devices utilizing advanced biodegradable materials.

In particular, its core technology is the SENS platform, which selectively delivers next-generation RNA-based therapeutics such as small interfering RNA (siRNA) and messenger RNA (mRNA) to specific target tissues.

Shortly after its relisting, at the end of last year, Samyang Biopharm was selected for a research project led by the Korea Drug Development Fund (KDDF) and entered into an agreement to jointly develop a candidate treatment for idiopathic pulmonary fibrosis (IPF).

The KDDF project aims to derive a preclinical candidate that suppresses regulators of pulmonary fibrosis pathology by expressing them in mRNA form, loading them onto the SENS platform, and selectively delivering them to lung tissue.

Samyang Biopharm has business supplying both active pharmaceutical ingredients and finished anticancer drugs domestically and overseas from manufacturing facilities that meet European and Japanese standards.

It also possesses biodegradable material synthesis technologies and is developing products across a wide range of areas, including surgical sutures, hemostatic agents, lifting threads, and polymer fillers.

As of the first half of last year, Samyang Biopharm recorded revenue of won 69.7 billion, operating profit of won 9.3 billion, and net profit of won 7.8 billion.

Copyright ⓒ 이데일리 무단 전재 및 재배포 금지

본 콘텐츠는 뉴스픽 파트너스에서 공유된 콘텐츠입니다.

다음 내용이 궁금하다면?

광고 보고 계속 읽기

원치 않을 경우 뒤로가기를 눌러주세요